In the “Great Rebuilding Era,” the global financial advisory and Wealth Management industry is experiencing one of the deepest structural transformations in its history. Coded for over a century as a “relationship-oriented,” “high-touch,” and personal trust-based profession, this sector is being redefined today by the transformative power of artificial intelligence (AI) and big data.

At the epicenter of this transformation, FINNY AI, a New York-based startup, is proving with its $17 million Series A investment that it is not merely a software company, but the architect of a new “organic growth” category.

The FINNY AI case aims to demonstrate how Vertical AI is “hacking” and rebuilding trillion-dollar industries. Our study maps the future of financial advisory from a broad perspective, stretching from the venture capital corridors of Silicon Valley to the regulation-laden offices of London, and from Singapore’s tech hubs to the dynamic fintech scene of São Paulo.

Part 1: The “Organic Growth” Crisis in Wealth Management and the Market’s Structural Deadlock

1.1. The Rainmaker Dilemma: The Time and Efficiency Paradox of Advisors

At the heart of the financial advisory profession lies a paradox that is difficult to resolve: The better an advisor serves their clients, the less time they have to find new ones.

In industry jargon, “Rainmakers”—super-advisors who consistently bring new assets to the firm—have always been a rare breed. However, today, this rarity has turned into a crisis.

According to Cerulli Associates and industry reports, 83% of Registered Investment Advisors (RIAs) view time constraints as the biggest obstacle to organic growth. In the traditional model, an advisor is forced to spend an average of 60 hours to convert a potential client (prospect) into an actual client. This 60 hours is time stolen from managing current clients’ portfolios, offering them tax strategies, or calming them down during market volatility.

Seth Godin’s “The Dip” theory comes into play here: Most advisors give up at this “dip” point brought on by the client acquisition process and rely solely on passive referrals. However, passive growth means the firm melts away during periods of inflation and market downturns. As FINNY AI founder Eden Ovadia realized during a job interview, even massive firms cannot rescue their advisors from this inefficient cycle, attempting to solve the growth problem by “hiring more people.” Yet, the problem is not a lack of human resources, but “process inefficiency.”

1.2. The Great Wealth Transfer and Changing Client Expectations

The world economy is witnessing a massive change of hands in capital, termed the “Great Wealth Transfer.” As the wealth of the Baby Boomer generation passes to Millennials (Gen Y) and Gen Z, client expectations are changing radically. For the new generation of asset owners, good returns alone are no longer sufficient. The set of expectations is being reshaped across three main axes:

Hyper-Personalization: Advice that is non-generic and makes them feel special.

Digital Speed: Instant response and transparency.

Proactive Approach: Offering solutions before the need arises.

Giant custodians like Schwab are complicating the participation requirements for advisor referral networks to keep up with this change and increase their own operational efficiency. For instance, Schwab raising the asset minimum required to enter its advisor network to $500 million has cut off the “ready client” tap for small and medium-sized firms. This situation forces firms to develop their own “hunting” capabilities—that is, to strengthen their “Outbound” marketing muscles. However, most advisors are financiers, not marketers. This is exactly where FINNY AI steps onto the stage to fill this talent gap.

1.3. The Market’s Quantitative Reality: Why Now?

Sequoia Capital’s “Act Two” thesis regarding the development of the AI market explains FINNY AI’s timing perfectly.

The first act (Act 1) was the rise of Foundation Models and general-purpose chatbots (ChatGPT, Claude). The second act is the application of these models to specific vertical sectors (Vertical AI), transforming them into “Agentic” systems that solve real business problems end-to-end.

FINNY AI is not a general sales tool; it is a specialized agent that understands the regulations (SEC, FINRA), terminology (401k rollover, tax-loss harvesting), and sensitivities of the wealth management industry. Market data confirms the appetite for such vertical solutions:

The Need for Organic Growth: 67% of advisors view organic growth as a top strategic priority.

High Client Value: The Lifetime Value (LTV) of a financial advisory client is measured in the tens of thousands of dollars. Therefore, any decrease in Customer Acquisition Cost (CAC) or increase in efficiency creates a leverage effect on the firm’s profitability (EBITDA).

Technology Adoption: According to a16z reports, financial services is one of the fastest-growing verticals in AI spending.

Chapter 2: FINNY AI – The Anatomy of a Category Creator and Technological Depth

2.1. Founder Vision: Redesigning Advisory via “First Principles”

The story of FINNY AI relies not on the classic narrative of “teenagers coding in a garage,” but rather on the diagnosis of a deep industrial problem with analytical intelligence. Founder CEO Eden Ovadia comes from a Boston Consulting Group (BCG) background. During his tenure at BCG, he worked in the Private Equity and Financial Institutions practice, essentially taking an “X-ray” of the sector from the inside. The reality Ovadia noticed during a job interview with a large RIA firm—“Advisors spend 70% of their time prospecting but conversion rates are very low”—ignited the spark for FINNY’s inception.

The founding team reflects the ideal “Hacker, Hipster, Hustler” balance of a modern technology startup:

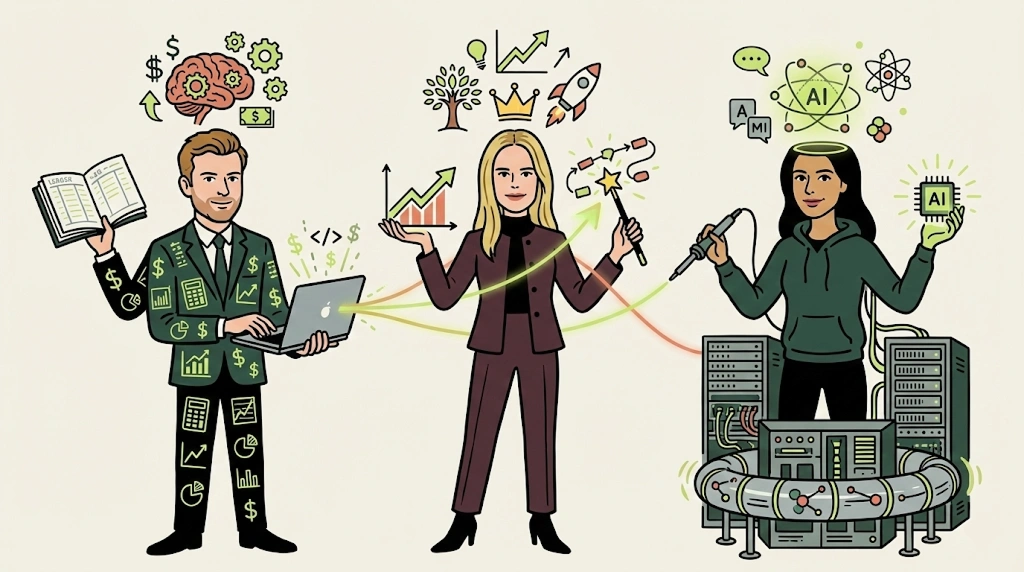

Eden Ovadia (CEO): Educated in Software Engineering and Machine Learning (ML) at McGill University and having developed his strategy muscles at BCG, he is a rare leader profile capable of reading both code and balance sheets.

Victoria Toli (President/CPO): Holds a degree in Artificial Intelligence and Symbolic Systems from Stanford University. A product leader with deep experience in “growth engineering,” having managed the growth strategies for the “Uber One” subscription product at Uber.

Theodore Janson (CTO): An Ecole Polytechnique and McGill graduate, an engineer pushing the boundaries of technology who has worked on LLM (Large Language Model) explainability and particle physics.

2.2. Product Architecture: F-Score, Intent Signals, and “Money in Motion”

FINNY AI’s core value proposition is positioned as a “marketing assistant for advisors that never sleeps, eats, or fears rejection 24/7.” However, this assistant is not a telemarketing robot making random calls, but a “growth engine” possessed of strategic intelligence.

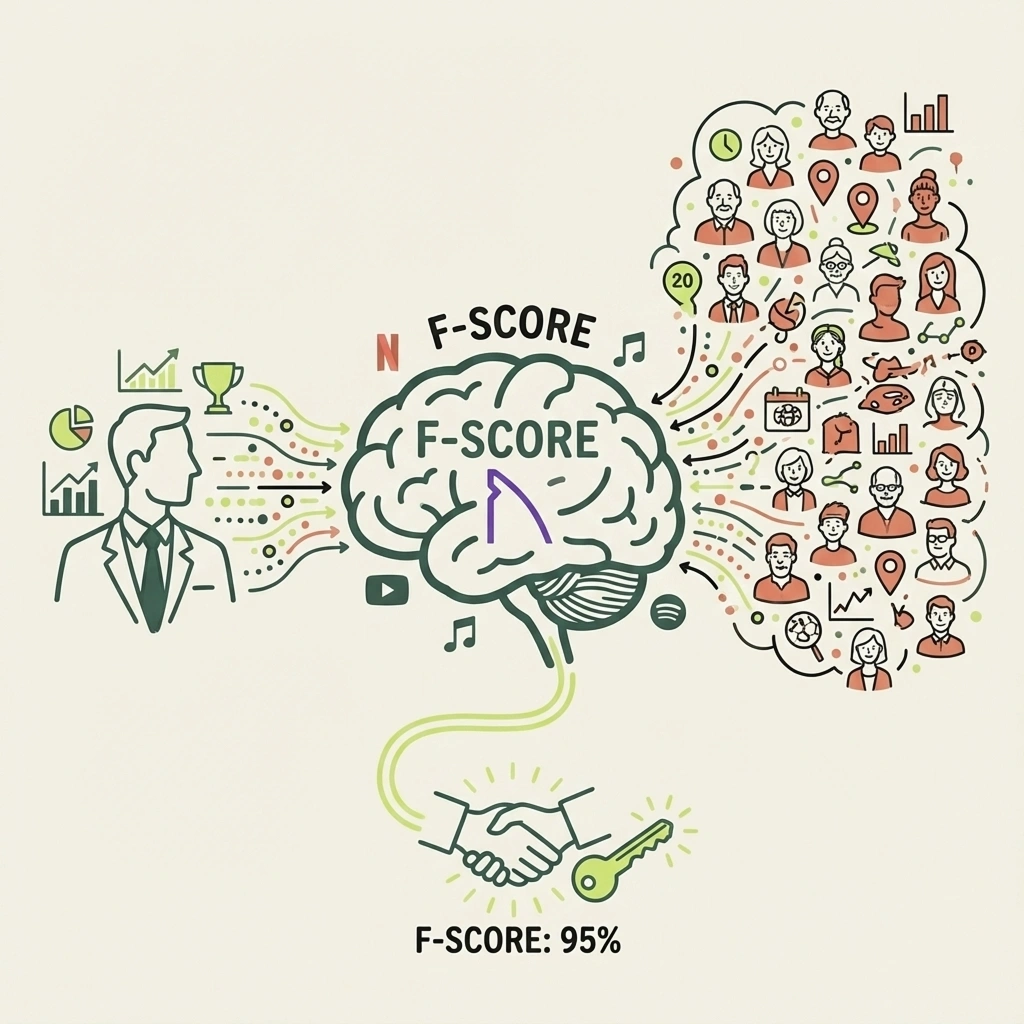

2.2.1. The F-Score Algorithm: Compatibility Score

FINNY’s brain is the F-Score (FINNY score) algorithm. This algorithm analyzes the financial advisor’s existing client profile (persona), areas of expertise, and past successes, matching them with potential prospects in the outside world. Just like Netflix’s movie recommendation engine or Spotify’s “Discover Weekly” playlist, the F-Score tells the advisor, “These are the people most inclined to work with you.” The algorithm processes thousands of data points.

Demographic Data: Age, location, occupation, education.

Financial Signals: Estimated net worth, income level.

Psychographic Data: Interests, investment preferences (e.g., ESG, crypto, real estate).

2.2.2. Detecting “Money in Motion”

In financial advisory, timing is everything. A person does not change their financial advisor or seek a new one unless a major change occurs in their life. FINNY captures “Money in Motion” signals, enabling the advisor to step in “Just-in-Time”:

Liquidity Events: A startup founder selling their company (Exit), an executive’s stock options expiring.

Career Changes: A C-Level executive changing jobs (requiring a 401k rollover), retiring.

Personal Events: Marriage, divorce, having children, receiving an inheritance.

FINNY detects these events from public data, news sources, and social media signals (LinkedIn changes, etc.) and alerts the advisor: “You need to speak with this person now.”

2.2.3. Intent Search and Multi-Channel Access

Beyond static data, FINNY scans 1.8 billion daily data signals with its Intent Search feature. When a potential client searches on Google for terms like “how to reduce estate tax” or “tax management in retirement,” this is an “intent” signal. FINNY identifies these high-intent candidates.

Subsequently, the system switches to Autonomous Outreach mode:

Personalized Emails: Writes messages that mimic the advisor’s tone, are non-generic, and refer directly to the candidate’s situation (e.g., their new job).

AI-Supported Voicemail Drops: Personal voice notes that sound as if they were produced by the advisor’s voice but can be left for thousands of people in a scalable way.

LinkedIn Automation: Sending connection requests and follow-up messages.

This process is conducted hands-free, without advisor intervention. The advisor deals only with “Hot Leads”—potential clients ready to buy who signify, “They want to meet with me.”

Part 3: Investment Analysis – $17 Million Series A and Strategic Signals

3.1. Smart Money’s Choice: Venrock and Strategic Angels

The $17 million Series A investment round announced in December 2025 is not merely a financial transaction, but also a validation of FINNY’s vision by industry giants. The round was led by Venrock. Founded in 1969 to manage the Rockefeller family’s wealth and invest in technology, Venrock is one of the “Blue Chip” firms of the venture capital world. As an early-stage investor in giants like Apple, Intel, and Check Point Software, Venrock’s leadership in FINNY serves as an indicator that the company is not just a “hype” product, but carries the potential for a deep industrial transformation.

Other names participating in the investment round essentially form a “Fintech All-Star Team”:

William McNabb (Former CEO of Vanguard): The legendary leader of Vanguard, the giant of passive investment and low-cost funds. McNabb’s participation demonstrates that FINNY is a critical tool not just for active managers, but for the entire wealth management ecosystem.

Jason Wenk (Founder and CEO of Altruist): The pioneer of modern, digital-first Custody. Wenk is one of the individuals who best understands how technology empowers advisors.

Y Combinator: FINNY’s birthplace and early-stage supporter. YC’s follow-on investment confirms its belief in the company’s growth trajectory.

Activant, Maple VC, Crossbeam Ventures: Funds specializing in B2B SaaS and vertical AI.

With this round, the company has raised over $20 million in total funding and pushed its valuation to the $150 million level. Metrics such as FINNY’s revenues increasing 50-fold since January 2025 and the clearing of its waitlist to begin serving over 400 firms underpin this high valuation.

3.2. Investor Perspective: Why FINNY?

Venrock partner Nick Beim’s words summarize the investment thesis: “FINNY combines deep technical expertise, product vision, and machine learning competence. This team represents the next evolution of advisor-centric technology.” Investors see the following in FINNY:

Proven Product-Market Fit (PMF): With 80% inbound demand and near-zero customer acquisition cost, the product demonstrates that it effectively sells itself.

Massive Total Addressable Market (TAM): Trillions of dollars in assets are managed in the US alone, and the churning or growth of these assets depends on the technologies advisors use.

Competitive Moat: Thanks to the data it collects and the feedback loop of the F-Score algorithm, FINNY transforms into a system that gets smarter the more it is used.

Part 4: Global Competitive Landscape – Global Examples and Comparative Analysis

Although FINNY AI is one of the brightest examples of a global trend (Vertical AI), it is not unique. Across different geographies of the world, there are similar or complementary startups shaped by local market dynamics, regulations, and cultural codes. It is critical for entrepreneurs interested in this space to understand this global landscape.

4.1. United Kingdom (UK): “Consumer Duty” and Compliance-Focused AI

The United Kingdom financial market is shaped by the Financial Conduct Authority’s (FCA) strict “Consumer Duty” regulations. Therefore, AI startups here focus on “compliance and correct advice” rather than “aggressive sales.”

Aveni.ai: This Scotland-based startup specializes in “Adviser Productivity” and “Compliance Automation.” While FINNY focuses on client acquisition, Aveni analyzes recordings of client meetings, detects risky phrases, and automatically prepares suitability reports. Since the admin burden on advisors in the UK is very heavy, tools like Aveni are of vital importance.

AdvisoryAI: With their AI assistants named “Evie” and “Emma,” they prepare meeting notes, suitability letters, and annual review reports. This is FINNY’s counterpart on the “admin” side.

Unbiased Pro: Unbiased, which is a marketplace, analyzes incoming leads for advisors with its AI feature called “SmartAccept” and automatically accepts them on behalf of the most suitable advisor, even outside of working hours. This is the marketplace version of FINNY’s “Intent Search” feature.

4.2. Continental Europe (Switzerland & Germany): Banking Secrecy and Hybrid Models

In Europe, GDPR and the culture of Banking Secrecy require a more cautious approach toward cloud-based AI solutions.

Unique.ai (Switzerland): Zurich-based Unique is developed specifically for the Private Banking sector. Running on the Microsoft Azure Switzerland cloud, the system places maximum importance on data security. Rather than finding clients externally like FINNY, Unique analyzes the bank’s existing data to offer “Investment Insights” and enables Relationship Managers (RMs) to approach the client better equipped. It also automates KYC (Know Your Customer) processes.

Datia (Sweden): In Scandinavia’s sustainability-focused market, Datia is an AI platform that analyzes and reports the ESG (Environmental, Social, Governance) compliance of portfolios. This is a critical differentiation point for advisors in Europe when “prospecting,” because European clients want to know the sustainability impact of their investments.

4.3. Asia-Pacific (APAC): “Super RMs” and Tech-Enabled Human Touch

In Asia, particularly in Singapore and Hong Kong, wealth management is growing rapidly, yet there is a shortage of qualified Relationship Managers (RMs). Technology here is used not to replace humans, but to “Augment” them.

IntellectAI (WealthForce.ai): Strong in India and Southeast Asia, this platform offers a “Hyper-Personalization” engine for RMs. Through ESG analytics, portfolio health checks, and “smart nudges,” it creates reasons for the RM to contact the client. Similar to FINNY’s “Money in Motion” logic, it tells the RM: “The client’s portfolio has entered a risk zone; call and suggest this.”

Paradino (Australia): The regulatory burden on financial advisory in Australia is one of the heaviest in the world. Paradino automates meeting notes and “Record of Advice” documents, saving advisors 5-10 hours a week.

4.4. Latin America (LatAm): Invisible Banking and WhatsApp Commerce

In Latin America, banking and financial advisory are conducted via mobile apps and messaging platforms rather than traditional branches.

Invisible Banking: Firms like Galileo Financial Technologies are making banking “invisible” via AI-supported background processes. For instance, when a client asks their voice assistant for the weather, the bank might adjust the energy budget in the background.

Conversational AI: WhatsApp usage in LatAm is over 80%. Therefore, for a tool like FINNY to be successful in this market, it must focus on WhatsApp integration rather than email. Digital banks like Nubank aggressively use AI in client acquisition for credit scoring and personalized offers.

4.5. North America (USA & Canada): FINNY’s Direct Competitors and Complements

While FINNY plays for leadership in the “Growth” category in the US market, there are strong competitors in the “Efficiency” space.

Catchlight: Backed by Fidelity, Catchlight is a lead scoring tool that scores the “conversion probability” of potential clients. It works on a similar logic to FINNY but focuses on providing insights to the advisor rather than the “autonomous outreach” (the agent sending emails itself) feature offered by FINNY.

Part 5: Marketing Philosophy

The secret sauce behind FINNY AI’s success is not just its technology, but the way this technology is marketed and positioned.

5.1. Trust Engineering and “Permission” Marketing

In his book “Permission Marketing,” Seth Godin discusses a process that transforms strangers into friends, and friends into customers. The traditional “Cold Call” is unpermitted and intrusive. FINNY overcomes this barrier by playing the “Relevance” card.

The Old Method: “Hello, I am a financial advisor, I would like to manage your money.” (Rejection rate 99%)

The FINNY Method: “Hello, I saw on LinkedIn that you sold your company. Congratulations. We implemented the [X] tax strategy with a client who went through a similar process. If you are interested, I can share the details.”

This approach combines McKinsey’s “Next Best Action” analytics with David Ogilvy’s principle of “Inform the client, don’t sell.” FINNY elevates the advisor from the position of a “salesperson” to that of a “value-adding expert.”

5.2. Advisor Psychology: Overcoming Call Reluctance

A financial advisor’s greatest enemy is not the markets, but the telephone receiver. “Call Reluctance” stems from the fear of rejection. FINNY takes this emotional burden off the advisor’s shoulders.

Artificial intelligence is immune to rejection, insults, or having the phone hung up on it. The advisor steps in only at the “positive” end of the process—that is, when a meeting request comes in. This keeps the advisor’s morale high and ensures they are more energetic and confident during client meetings.

5.3. Tribes and Niche Marketing

As Godin states in his book “Tribes,” people want to belong to communities that are like themselves. FINNY helps advisors find their “Niche” audiences. For example, specific segments like “Advisor for Tech Executives” or “Financial Planner for Divorced Women” become targetable thanks to FINNY’s data capabilities. Instead of casting a wide net, hunting with a laser-focused harpoon dramatically increases conversion rates.

Part 6: Strategic Lessons for Entrepreneurs (The Playbook)

FINNY AI is one of the most successful applications of Y Combinator’s (YC) recent “Vertical AI” thesis. The critical lessons entrepreneurs can draw from this case are as follows:

6.1. Vertical Depth, Not Horizontal Breadth (Vertical Depth > Horizontal Breadth)

Many AI startups make the mistake of trying to build a “Sales Assistant for Everyone” (Horizontal AI). FINNY focused solely on the “Financial Advisors” vertical. What did this gain them?

Domain-Specific Data: They were able to train a model that learned the sector’s regulations (Reg BI, SEC rules) and terminology.

Trust: They were able to attract “Strategic Angels” from within the industry (McNabb, Wenk, Brown) as investors. If they were a general sales tool, the former CEO of Vanguard wouldn’t have been interested.

Pricing Power: Vertical solutions can always be priced higher (Premium Pricing) than general solutions.

Lesson: Narrow your niche so much that you are the “only” solution in that space.

6.2. “Do Things That Don’t Scale” vs. “Automate Everything”

Paul Graham‘s famous advice, “Do Things That Don’t Scale,” applies to the beginning. However, FINNY has taken something unscalable (building human relationships, writing letters, leaving voicemails) and made it “scalable” via AI.

Entrepreneurs should seek out processes where human labor is a bottleneck, yet the human touch is essential. FINNY has solved a seemingly impossible paradox: “Automating Empathy.”

6.3. Founder-Market Fit

The FINNY team used the “Team” as one of the strongest slides in their investor presentations (Pitch Deck). The CEO’s BCG and finance background, the President’s Uber and growth background, and the CTO’s deep AI background. This combination sends the following message to the investor: “The experience and passion to best solve this problem are right in front of me.”

Lesson: Position your past experiences as an “unfair advantage” that legitimizes your startup.

6.4. Ecosystem Partnerships

Instead of fighting alone, FINNY followed a strategy of integrating with the giants of the ecosystem (custodians, broker-dealers, other technology providers).

Relationships established with firms like Orion and Integrated Partners opened the distribution channel. In the B2B world, distribution is as important as the product.

Part 7: Future Perspective – The Rise of Agents and the 2030 Vision

7.1. The Agentic Era

The 2024-2025 period was the “Co-pilot” era; the human initiated, and AI assisted. 2026 and beyond will be the “Agent” era. FINNY is the pioneer of this transition. In the future, FINNY will not just set meetings, but will also:

Request and collect necessary documents from the client.

Draft a basic financial plan.

Fill out account opening forms.

Give the order to send flowers on the client’s birthday.

The advisor will not be the “operating system” of the process, but its “decision maker” and “emotional anchor.”

7.2. The Risk of Commoditization and the Human Factor

As artificial intelligence evolves, technical tasks like “asset allocation” and “portfolio management” will become completely commoditized. Tools like FINNY democratize not these technical tasks, but the ability to “find and persuade humans.” However, this brings a risk: If everyone uses the same AI tools, what will create the difference?

Answer: Brand and Trust. FINNY will save advisors time to build their “Personal Brands.” The winning advisors of the future will not be those who use the best algorithm, but those who use the time created by that algorithm to build deep bonds with their clients.

7.3. Regulation and “AI Washing”

The SEC and other regulatory bodies are becoming increasingly sensitive regarding “AI Washing” (pretending to use AI when not, or exaggerating AI capabilities).

Firms like FINNY will need to be transparent about how their algorithms work, how they use data, and how they prevent bias (“Explainable AI”). In the future, “AI Audit” will become as standard a procedure as financial auditing.

Conclusion: A New Operating System

FINNY AI’s $17 million investment is a turning point. This is the official declaration of the financial advisory sector’s transition from the era of “Excel spreadsheets and golf course chats” to the era of “Data signals and algorithmic empathy.”

FINNY promises advisors this: “Focus on being human, leave the rest to the machine.”

Because this promise solves the biggest bottleneck (time and growth) in a trillion-dollar industry, FINNY and similar “Vertical AI” startups are candidates to be the biggest success stories of the coming decade. The message for entrepreneurs is clear: Find large, boring, regulated, and inefficient industries; and inject not just software, but “intelligence” into them.

Sources and References

FINNY Gets $17 Million Series A to Define ‘Automated Organic Growth’ -(https://riabiz.com/a/2025/12/24/finny-gets-17-million-to-define-category-automated-organic-growth-for-rias-with-major-enterprise-deals-up-next-and-80-inbound-calls)

The Cerulli Report: U.S. RIA Marketplace 2025 – Cerulli Associates

The Diamond Podcast: How AI Is Powering the Next Era of Advisor Growth (Interview with Eden Ovadia) -(https://www.diamond-consultants.com/the-future-of-prospecting-how-ai-is-powering-the-next-era-of-advisor-growth/)

Generative AI’s Act Two -(https://sequoiacap.com/article/generative-ai-act-two/)

The AI Application Spending Report – Andreessen Horowitz (a16z)

YC Company Profile: FINNY AI -(https://www.ycombinator.com/companies/finny-ai)

FINNY Launches: Supercharge Organic Growth for Financial Advisors -(https://www.fondo.com/blog/finny-launches)

Wealth Management EDGE Speaker Profile: Victoria Toli – Informa Connect

FINNY: Unlocking Organic Growth in Wealth Management – Venrock Insights

AI Startup FINNY Raises $17M for Advisor Prospecting Push -(https://www.techrepublic.com/article/news-ai-startup-finny-funding/)

FINNY Unveils Intent Search to Help Advisors Pinpoint High-Intent Prospects -(https://www.businesswire.com/news/home/20250609899894/en/FINNY-Unveils-Intent-Search-to-Help-Advisors-Pinpoint-High-Intent-Prospects-Faster)

FINNY Closes $17 Million Series A Funding Round – Morningstar

Aveni.ai – AI for Financial Services – Aveni.ai

AdvisoryAI – AI Tools & Software for Financial Advisers – AdvisoryAI

Unbiased Pro Launches SmartAccept AI Growth Assistant – Unbiased

Unique.ai – Agentic AI for Financial Services – Unique.ai

Datia – Sustainable Finance Data Platform -(https://www.datia.app/)

IntellectAI – WealthForce.ai – IntellectAI

Paradino – AI Automation for Financial Advisers – Paradino.ai

Invisible Banking: LatAm Adoption 2026 -(https://www.galileo-ft.com/blog/invisible-banking-latam-adoption-2026/)

Use Cases of Generative AI in LatAm Payments – PaymentsCMI

Jump – The AI Assistant for Financial Advisors – Jump.ai

Best AI Notetakers for Financial Advisors 2025 -(https://wealthtechtoday.com/2025/04/29/best-ai-notetakers-for-financial-advisors-2025-a-strategic-buyers-guide/)